Key Insights for Australian Businesses from a Landmark Report

ASX: Navigating the Climate Reporting Tide

Andrew Douglas, Director, Opportune

21 August 2025

The mandatory reporting and assurance requirements under AASB S2 and ASSA 5000 represent one of the most significant shifts in corporate reporting in a generation. Understanding where ASX-listed entities currently stand is crucial for your own preparedness.

That's why I'm excited to share a plain English summary of a pivotal joint research report from the Australian Accounting Standards Board (AASB) and Auditing and Assurance Standards Board (AUASB), titled "Preparedness of ASX-listed entities for climate-related reporting and assurance requirements: Trends in Annual Report Disclosures in 2023 and 2024". This report, authored by Dr Jean You, Yi She, Professor Roger Simnett, and Associate Professor Shan Zhou, offers timely and invaluable insights into how ASX-listed companies are preparing for these changes.

The report's analysis of Annual Report disclosures in 2023 and 2024 serves as a critical pulse check before AASB S2 Climate-related Disclosures and ASSA 5000 General Requirements for Sustainability Assurance Engagements come into full effect. It highlights the growing recognition among Australian listed entities of the importance of disclosing climate-related impacts and the financial implications thereof.

The original report can be located here: https://aasb.gov.au/media/wuvl5ckt/aasb_auasb_rr_climatereporting_07-25.pdf

Key Findings from the Report

The research paints a clear picture of increasing, though varied, preparedness across ASX-listed entities.

Here are the standout findings:

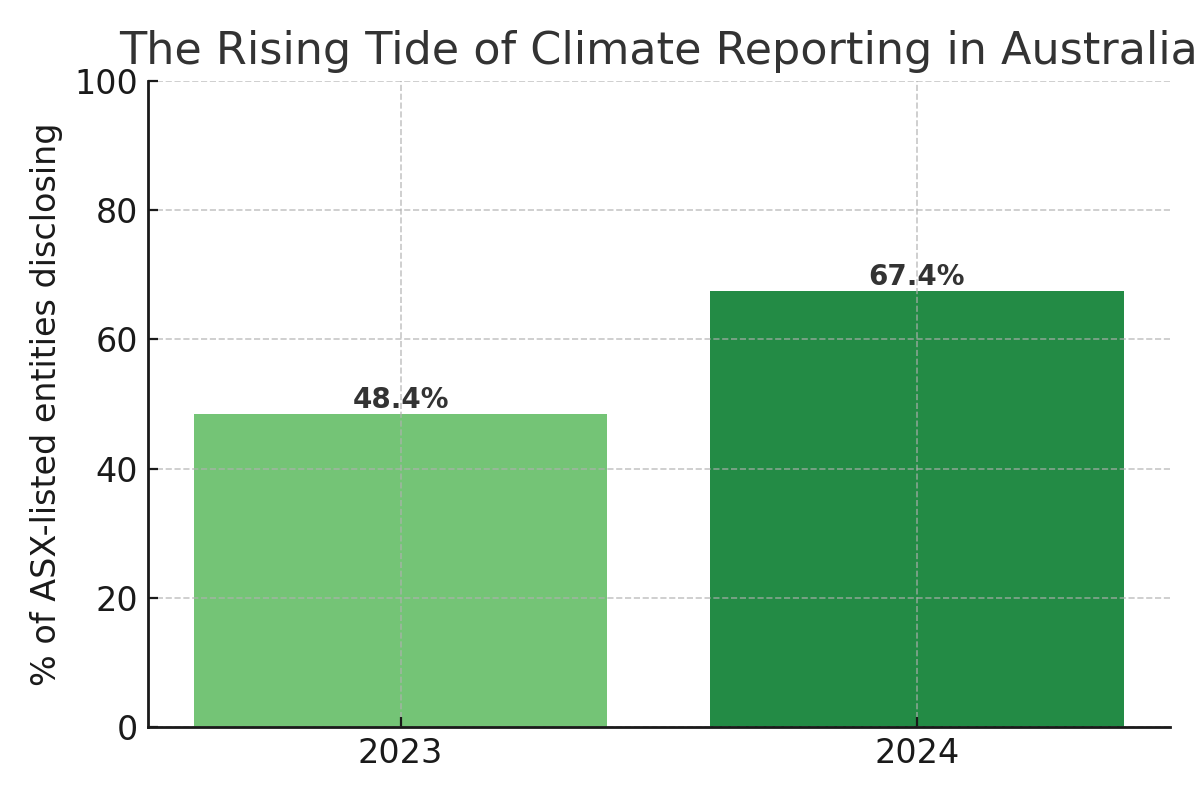

• Significant Uptick in Disclosure: The overall rate of ASX-listed entities including climate-related information in their Annual Reports jumped from 48.4% in 2023 to 67.4% in 2024. This demonstrates a broad industry-wide move towards enhanced climate reporting.

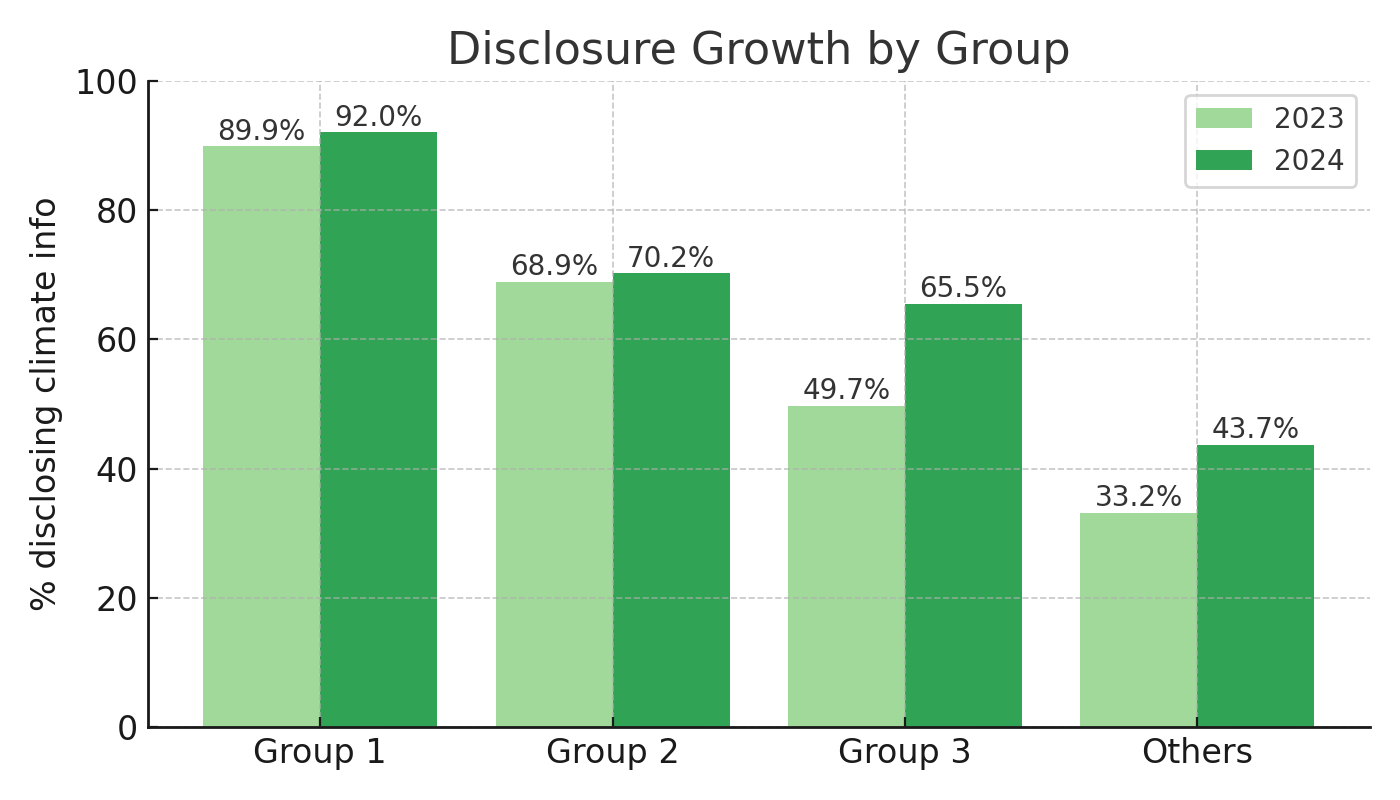

• Group 1 Entities Leading the Charge: Group 1 listed entities, those first in line for mandatory reporting, are highly prepared, with over 90% (92.0% in 2024) already disclosing climate-related information. This indicates strong proactivity within this group.

• Industry-Wide Progress: While climate-sensitive industries naturally show higher disclosure rates, increases were observed across all industry groups. Notably, the Health Care sector experienced the most significant improvement, despite starting from a lower base.

• Growing Alignment with AASB S2: There’s an increasing awareness of and referencing to Australian Sustainability Reporting Standards or IFRS Sustainability Disclosures Standards (from 12.6% in 2023 to 18.3% in 2024). The adoption of the four core content areas of AASB S2 (Governance, Strategy, Risk management, and Metrics and targets) also rose, from 7.9% to 12.7% of disclosers.

• Scenario Analysis is Emerging: Disclosures of scenario analysis in Annual Reports, a key requirement for assessing climate resilience and risk management, increased from 7.1% to 11.7% of disclosers. Most analyses relate to global warming/temperature changes, often using three scenarios.

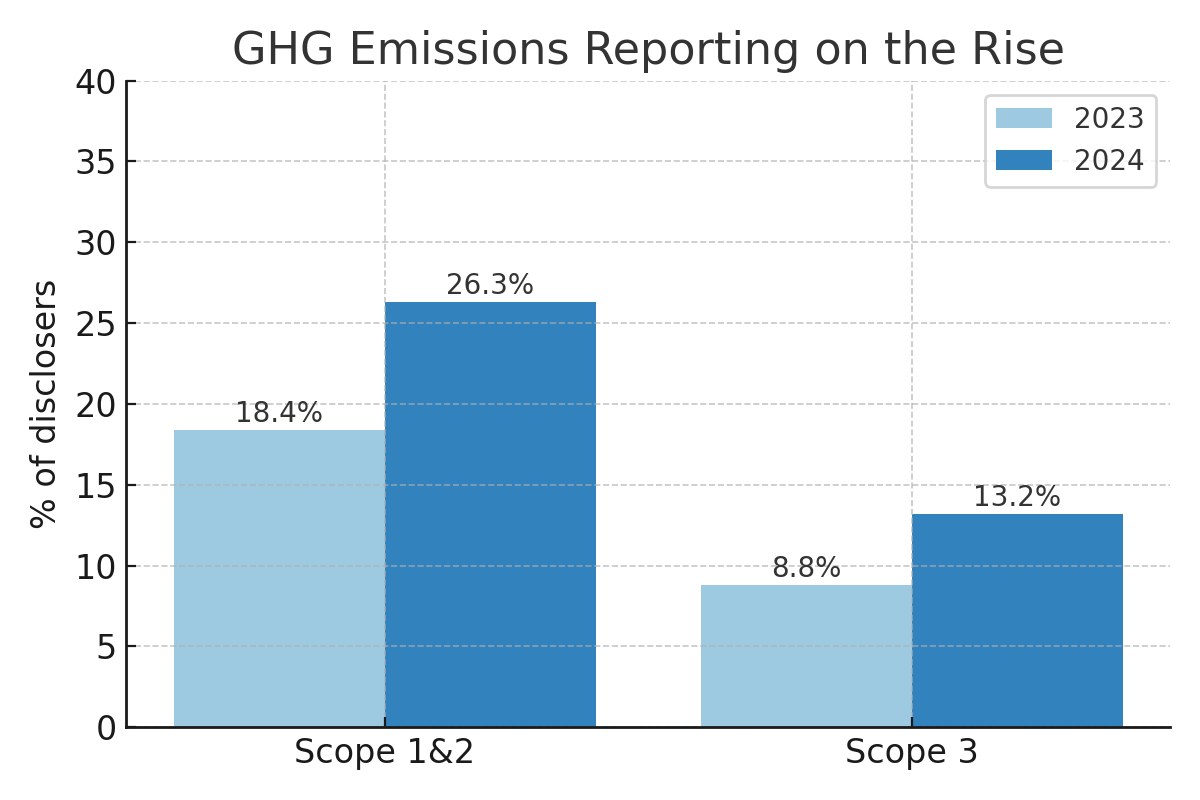

• GHG Emissions Reporting on the Rise: The proportion of entities disclosing Scope 1 and Scope 2 GHG emissions showed an upward trend (18.4% to 26.3%), and Scope 3 GHG emissions disclosures also increased (8.8% to 13.2%). However, Scope 3 disclosures remain about half that of Scope 1 and 2, highlighting room for improvement in value chain emissions reporting.

• Climate-Related Incentives in Remuneration: A growing percentage of listed entities are incorporating climate-related incentives or performance assessments into their Remuneration Reports, rising from 9.9% to 14.6% of disclosers. This shows a rising emphasis on linking executive compensation to climate objectives.

• Climate in the Financial Notes: The inclusion of climate-related information in the Notes to the Financial Statements increased from 17.5% to 23.3% of disclosers, demonstrating a growing awareness of climate-related financial impacts. "Accounting policies, judgments or basis of preparation" and "Auditor's remuneration" were key areas.

• Auditors Integrating Climate: A small but increasing number of Auditor’s Reports are including climate-related impacts in Key Audit Matters (KAMs), primarily related to Asset valuation. The Big 4 firms are dominant here.

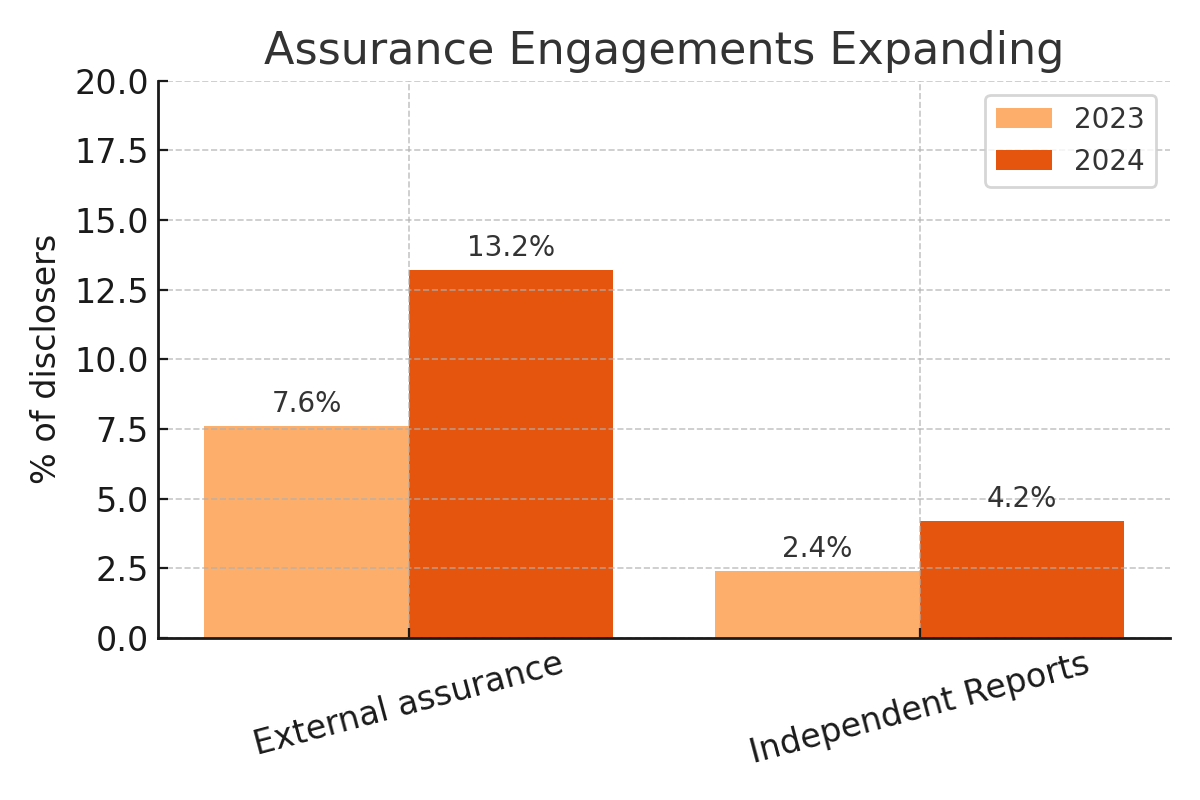

• Assurance Engagements are Expanding: There's a notable increase in listed entities referencing third-party assurance engagements on climate-related information (from 7.6% to 13.2% of disclosers) and including Independent Assurance Reports (from 2.4% to 4.2%). While limited assurance remains most common (76%), the use of combined limited and reasonable assurance is on the rise (24%), a positive step towards the reasonable assurance target by 2030. GHG emissions are a primary subject matter for these assurance engagements.

Key Areas for Continued Focus

While the report doesn't explicitly list "recommendations" from the Boards, its findings clearly highlight areas where businesses need to enhance their efforts to fully meet the spirit and letter of the upcoming requirements:

• Deeper AASB S2 Integration: Continue to move beyond simple disclosure towards a fully structured and comprehensive approach aligned with all four core content areas of AASB S2.

• Robust Scenario Analysis: Expand the scope and sophistication of scenario analysis to genuinely assess climate resilience and embed it within strategic planning and risk management.

• Comprehensive Scope 3 Reporting: Address the lag in Scope 3 GHG emissions reporting. Understanding and disclosing these value chain emissions is critical for a holistic climate impact assessment.

• Enhanced Financial Connectivity: Strengthen the link between sustainability disclosures and financial reports. More guidance may be needed to ensure climate impacts are appropriately reflected within the Financial Reports themselves, rather than predominantly outside them.

• Progression to Reasonable Assurance: Actively work towards achieving reasonable assurance for climate-related disclosures as the mandatory timeline approaches. This builds greater confidence and reliability.

• Standardised Reporting Criteria: Move away from self-developed methodologies towards globally recognised frameworks like the GHG Protocol and GRI for consistency and comparability.

Practical Learnings You Can Apply

For your business, whether you’re an ASX-listed entity or preparing to be one, these findings offer actionable insights:

• Don't Procrastinate – Act Now: The mandatory reporting and assurance requirements are not distant future events; they are upon us. The strong preparedness of Group 1 entities underscores the advantage of early adoption. Start your preparation if you haven't already.

• Embrace AASB S2 as Your Blueprint: Familiarise yourself deeply with the four core content areas of AASB S2: Governance, Strategy, Risk Management, and Metrics and Targets. Structure your climate-related disclosures around these pillars to ensure comprehensive reporting.

• Master Your Emissions Data, Especially Scope 3: Invest in robust systems for measuring and reporting all scopes of GHG emissions – Scope 1, 2, and critically, Scope 3. This is an area where many are still catching up, and it represents a significant portion of an entity's climate impact.

• Integrate Scenario Analysis into Strategy: Beyond a compliance checkbox, use climate scenario analysis to truly understand potential climate-related risks and opportunities for your business. This foresight is crucial for long-term strategic resilience.

• Bridge the Gap Between Climate and Finance: Work closely with your finance teams and auditors to identify and appropriately reflect climate-related financial impacts within your financial statements. This connectivity is vital for investor confidence and regulatory compliance.

• Plan for Assurance from Day One: Don't view assurance as an afterthought. Engage with experienced third-party assurance providers early. Starting with limited assurance is a good step, but understand the roadmap towards reasonable assurance and build your internal processes to support it.

• Align Executive Incentives with Climate Goals: Consider how linking executive remuneration to climate performance metrics can drive accountability and accelerate progress towards your climate objectives.

• Leverage Established Frameworks: Where possible, adopt and apply internationally recognised reporting frameworks like the GHG Protocol, GRI, and NGER scheme. This will enhance the credibility and comparability of your disclosures.

The journey towards comprehensive climate-related reporting and assurance is an ongoing one. This report provides a valuable benchmark for Australian businesses. By understanding these trends and applying the learnings, you can not only meet your compliance obligations but also strengthen your business’s resilience and reputation in a climate-conscious world.

Stay tuned to our blog for more updates and deeper dives into the specifics of climate accounting and auditing!

Andrew Douglas, Director